Table of contents

Introduction

Insurance has mature models for storms, quakes, and wildfires, but the most persistent losses in infrastructure rarely come from the hazards everyone talks about; they start beneath the ground.

None of these are edge cases. They are the kinds of failures that show up again and again across warehouses, data centers, logistics parks, energy corridors, and public infrastructure - losses insurers often inherit long after a project has been completed.

The challenge isn’t that the ground is unpredictable. The challenge is that insurance workflows were never built to evaluate it. Subsurface risk remains one of the least modelled hazards, not because it’s impossible to measure, but because the evidence required to understand it has never existed in a form insurers can use: early, scalable, structured, contextual, and auditable.

Meanwhile, the world that insurers support is changing fast. Infrastructure and hyperscale construction are being built at a record pace. Risk engineering teams are stretched thin. Climate-driven soil and groundwater volatility are reshaping how the ground behaves.

The gap is widening.

Insurers are being asked to underwrite tomorrow’s complexity with yesterday’s knowledge and tools.

Why Ground Stability Risks Remain Unmodeled in Insurance

Most insurance policies exclude subsidence, soil compression, and differing site conditions entirely. Because the information received is partial or unreliable, it is a complex task to understand where these risks are emerging or how they evolve. Without a trusted, multi-year context, subsurface risks become an unquantifiable exposure, and it’s therefore easier to exclude them than to price them in.

The challenge is that subsurface issues don’t stay neatly confined to “subsidence.” The same underlying conditions can trigger a range of events that are covered: slab cracking, utility damage, road/highway deformation, drainage failure, structural movement, and third-party liability.

Insurers end up exposed to the consequences of ground instability, while having limited visibility into the causes. Let’s look at the challenges one by one.

Sparse Primary Data

Every submission ultimately depends on a handful of boreholes and a geotechnical report. Those boreholes are accurate at the exact points where they’re drilled, but they don’t address the wider area picture. They don’t capture how the bearing layer changes 20-30 meters away, how groundwater moves through the season, or whether a section of the site sits on undocumented fill.

Most importantly, the consistency isn’t there. Two underwriters reading two different geotechnical reports for similar sites can walk away with entirely different interpretations. Formats and levels of detail vary, and the data density is almost always too thin to support confident underwriting.

Decisions end up relying on professional intuition, not spatial visibility.

Fragmented, Non-Uniform Evidence

A typical submission arrives with scattered information:

- bore logs

- grading and levelling plans

- CAD drawings

- inspection notes

- drone photos

- soil lab results

- 150–300-page PDF reports

- environmental records

None align to a common format. None flow into a unified pipeline.

Underwriters and engineers routinely spend considerable amounts of time piecing together basic facts about what the site is, how it has evolved, and what might be hiding below the surface.

No Unified, Multi-Year View of Ground Behavior

Perhaps the biggest gap: insurers rarely have the opportunity to understand how the ground actually behaves over months or years.

There’s no multi-year deformation record.

No history of terrain modification or legacy earthworks.

No visibility into groundwater recharge or seasonal shifts.

No ability to compare pre-event and post-event conditions during a claim.

No way to verify claims rooted in “pre-existing conditions.”

Without these temporal layers, insurers are left making judgment-based decisions about risks that unfold over years or decades. That’s the heart of the problem: the current workflow doesn’t address ground stability risk with continuous evidence.

Insurance Workflows Need An Upgrade

When a submission comes in, the underwriting process looks straightforward on paper:

- The broker sends documents.

- The underwriter screens the package.

- A risk engineer reviews the technical material.

- Additional information is requested.

- A consultant interprets the evidence.

- Everything circles back for final pricing and conditions.

But in practice, it’s complex. Underwriters start with partial information. Risk engineers are handed dense reports and unstructured documents without a clear risk summary of the site. Consultants provide point-in-time interpretations based on limited evidence. Throughout this loop, site stability risks remain inconsistent or scattered.

The strain is amplified by rapid additions to the portfolio as construction projects expand faster than ever. One engineer may be reviewing dozens of complex sites each week, leaving little room for deep analysis.

The global market for Data Center Construction was at US$245 B in 2024 and is projected to reach US$371 B by 2030, growing at a CAGR of 7.2%.

- BusinessWire

At the same time, climate variability is shifting groundwater patterns, intensifying shrink-swell cycles, and changing the behavior of soft soils that static reports cannot capture. Insurance is facing more ground-related losses with less capacity to evaluate them. And there are repercussions that insurers face:

- Triage slows down when submissions are messy

- Inconsistent underwriting due to varying interpretations

- Engineering reviews become expensive or repetitive

- Exposures are accepted without full visibility

- Unnecessary declines

- Disputes over “differing site conditions”

The need is clear on all ends. Insurers want speed. Engineers want accuracy. Compliance wants traceability. Traditional workflows force trade-offs among all three.

Loss Patterns: What Claims Data Reveal

Across liability and first-party portfolios, insurers encounter the same ground-related issues year after year. The terminology may differ, the assets change, but the underlying reasons stay the same.

“It can take years to conclude whether the policy was profitable”

Failures emerge gradually, sometimes long after a building has been handed over. By the time they show up as damage or third-party liability, the dispute has already arisen between the parties.

- Did the issue already exist, or did it emerge later?

Without pre-bind evidence of ground behavior, insurers are forced to navigate these disputes with a slow, costly, and often inconclusive process.

Existing Tools Each Solve a Fragment of the Problem

For insurers, the issue isn’t just a lack of inputs. It’s the absence of a single, auditable evidence layer that brings everything together: the specificity of borehole logs, the insights buried deep in submitted documents, and their correlation with real-world data from wide-area ground motion, water risk, and historical changes.

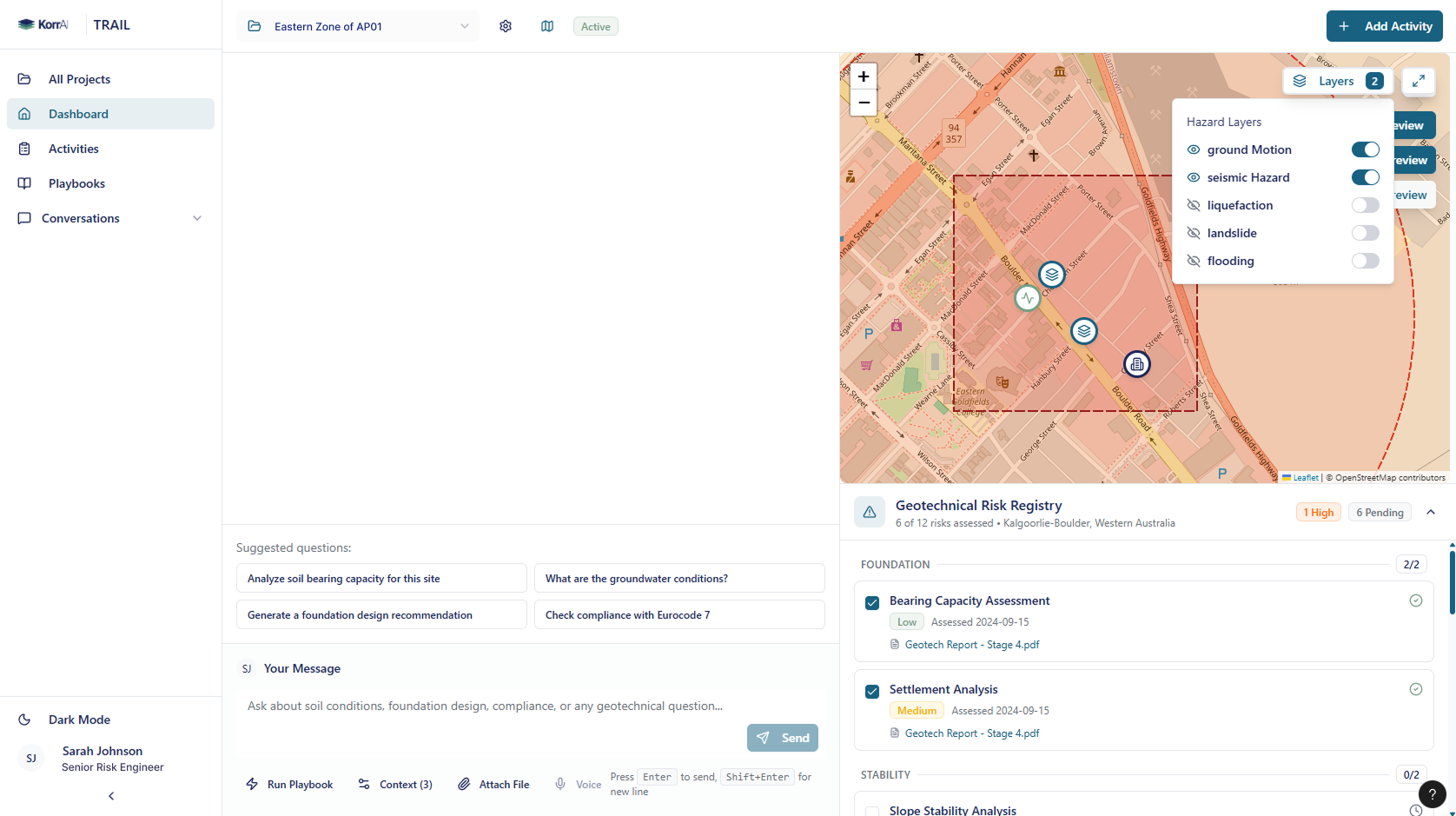

Introducing TRAIL Playbooks for Insurance Workflows

What is TRAIL for Insurance?

TRAIL is an AI co-worker for insurers. It’s an agent that reads all the dense reports and unstructured documents, interprets satellite-derived ground motion maps, cross-references multi-hazard layers, and assembles all of it into an underwriting-ready package with clear, traceable reasoning.

It helps the underwriting team skip days of document hunting. It enables the claims team to evaluate site conditions without on-site inspections to verify claims.

Using TRAIL playbooks, they can find the critical signals for insurance-ready analysis.

What are TRAIL Playbooks?

Playbooks are standardized workflows inside TRAIL that assess different risk aspects. Each playbook is built on measured, multi-year geospatial evidence delivered through source-backed summaries, risk classes, and maps that directly support underwriting, engineering referral, and claims analysis.

{{services-widget}}

How Playbooks Support Underwriting to Claims

TRAIL Playbooks strengthen the existing insurance workflows. For construction liability and large infrastructure projects, they provide underwriters, risk engineers, and claims teams with a single, consistent evidence layer they can rely on from first submission to post-event analysis.

Underwriting & Engineering Referral

Playbooks give underwriters and risk engineers a clear, consolidated view of ground stability, grading history, and water-related sensitivities around a proposed project. Instead of scanning scattered documents or relying on isolated boreholes, the team sees:

- mapped stability trends

- areas of subsurface variability

- water-driven accumulation or recharge zones

- portions of the site shaped by past earthworks

This helps sharpen early decisions: when to request more information, when to apply conditions, and when to escalate for engineering review. More importantly, it provides traceable justification for those decisions, grounded in measurable evidence rather than judgment alone.

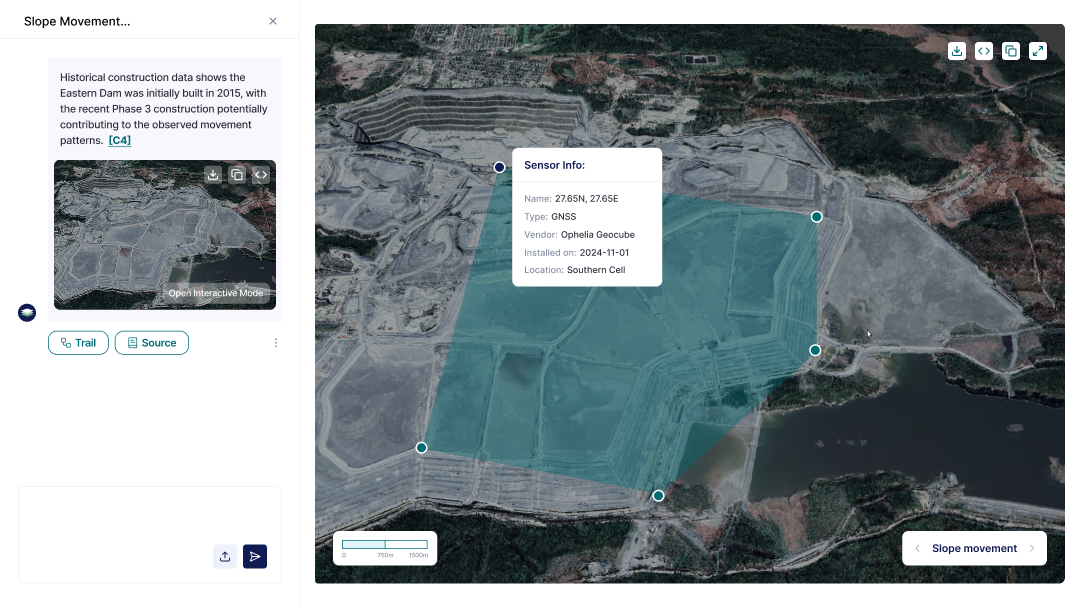

Claim Auditing & Forensic Engineering

When ground-related disputes arise years after construction, settlement, uplift, drainage failures, or neighbor impact - Playbooks help reconstruct what the site looked like before, during, and after the project.

This includes:

- Pre-existing deformation and water risk

- How earthworks or grading changed the terrain

- Whether movement patterns accelerated post-construction

- Which conditions were foreseeable at bind

The ability to compare pre- and post-event ground behavior gives claims teams a neutral evidence baseline for determining whether the loss stemmed from pre-existing conditions, construction activities, or external factors. It shortens disputes, clarifies responsibility, and supports more defensible outcomes.

Case Study: How KorrAI Helps Zurich’s Construction Liability Underwriting

Context

Zurich E&S provides a tangible example of how remote ground intelligence is already reshaping underwriting. Within Construction Liability, Zurich operationally uses KorrAI’s Ground Motion Risk Index (GMRI) as part of its risk-enrichment workflow. While subsidence is excluded under Property as part of Earth movement, it remains a significant third-party liability exposure for contractors, design-build firms, and engineers.

This is where pre-bind visibility has been thin for a long time.

Solution

To address this gap, Zurich integrates GMRI directly into its Statement of Values (SOV) enrichment pipeline. GMRI is appended for eight high-risk states where ground movement has been shown to materially influence liability outcomes.

This expanded evidence stack feeds into Zurich’s Casualty Risk Quality Score, which informs escalation pathways. GMRI effectively becomes a structural part of the decision process: a way to quickly identify sites with elevated ground instability and to ensure that referrals and conditions are grounded in measurable risk rather than anecdotal interpretation.

Impact

GMRI inside Zurich’s workflow has served as consistent evidence for construction liability underwriting. Zurich’s deployment validates GMRI as insurer-grade, operational, and scalable.

With TRAIL Playbooks, Insurers can move from a single powerful signal to a fully structured evidence layer to provide consistent, documented, and defensible underwriting.

Final Thoughts

Subsurface risk has always been present; what’s been missing is a reliable way to see it early, accurately, and at the scale insurance demands. GMRI proved that multi-year ground evidence can meaningfully strengthen construction liability decisions. TRAIL and its Playbooks build on that foundation, bringing document intelligence, site evolution, groundwater behavior, and hazard context into one traceable workflow.

For insurers navigating rapid construction growth and rising ground-related losses, this represents a practical way forward: clearer visibility, more consistent decisions, and better control of long-tail exposure.

If you’d like to explore how TRAIL can support your underwriting and risk engineering programs, you can submit an expression of interest for TRAIL or book a meeting with our experts to learn more.

Share this post

Written By

.png)

Rahul Anand

PDG et cofondateur

Rahul est PDG et cofondateur de KorrAI. Entrepreneur en série, il a déjà bâti des entreprises prospères dans les secteurs de l'Internet grand public et de l'IoT. Il vise maintenant à lutter contre l'affaissement du sol, qui devrait toucher plus de 25 % de la population mondiale au cours des prochaines décennies.

Rob McEwan

CPO et cofondateur

Rob dirige le développement de produits chez KorrAI, se spécialisant dans l'InSAR, la télédétection et l'analyse géospatiale pilotée par l'AI. Avec une formation en géologie et en science des données, il a travaillé dans les domaines de l'exploration, de l'exploitation minière et de l'analyse basée sur le SIG. Passionné par la technologie et la créativité, il aime la photographie infrarouge, la musique et les projets pratiques en menuiserie et en automatisation.

Written By

Team KorrAI

Ground Motion Risk Index (GMRI)

Piling Risk

Water & Drainage Risk

Site Evolution

Document Intelligence

Nous envoyons à l'occasion des courriels contenant des mises à jour, nos derniers blogues et nos lectures préférées sur InSAR et le paysage lent de l'affaissement du sol.

Abonnez-vous à notre infolettre

Lu par les meilleurs professionnels sur

.png)

Je vous remercie ! Votre soumission a bien été reçue !

Oups ! Quelque chose s'est mal passé lors de la soumission du formulaire.

.png)

KorrAI identifie les menaces que représentent les mouvements au sol pour les infrastructures essentielles à l'aide des données InSAR provenant de satellites et de réseaux de capteurs au sol.

Droit d'auteur

.svg)

2025 KrAi